Case Study: How Paays built a one-of-a-kind travel lending experience

Adaptiv Admin

Mar 27, 2026 · 11 min read

Executive Summary

In 2019, millions of Canadians wanted to travel. Most of them didn't. Not because the desire wasn't there, but because the budget wasn't ready. Paays set out to fix that with PreQ: a pre-qualified travel loan embedded directly into the booking journey, available at the moment of inspiration rather than the moment of desperation.

PreQ surfaced a borrowing amount before the user picked a destination. It integrated live flight and hotel inventory through Expedia. It verified income in the background through open banking via Flinks, so approval felt instant. And it layered exclusive partner deals on top of the financing, so Paays users didn't just get a loan, they get a better price on the trip itself.

The result was a product that transformed travel financing from a last resort into a first step.

The Challenge

The travel purchase decision is almost entirely emotional. A photo on Instagram, a deal in an email, a friend who just got back from somewhere wonderful - these are the real triggers. And they happen fast.

Traditional travel financing doesn't. Applying for a loan mid-booking means leaving the experience, submitting documents, waiting for a decision, and hoping the fare hasn't moved by the time you return. By the time the approval arrives, the motivation is gone.

Three specific failure modes defined the problem:

Discovery fragmentation. Users encounter travel inspiration across social media, comparison platforms, and email newsletters, but no financing option is present in those surfaces. The moment of desire and the moment of funding never meet.

Pre-approval anxiety. Most lenders only reveal what you can borrow after a hard credit check. That's a high-commitment ask for someone who's still just browsing. It turns exploration into a formal application, and many users walk away before they start.

Journey interruption. When users do attempt to finance mid-booking, the process routes them out of the travel experience entirely. They lose their session, their selected trip, and often their resolve.

"By the time the loan is approved, the trip they wanted is sold out, more expensive, or emotionally cold."

The people most affected by this weren't irresponsible borrowers; they were simply ordinary travellers with steady incomes and genuine intent, caught in the gap between when inspiration strikes and when money is available.

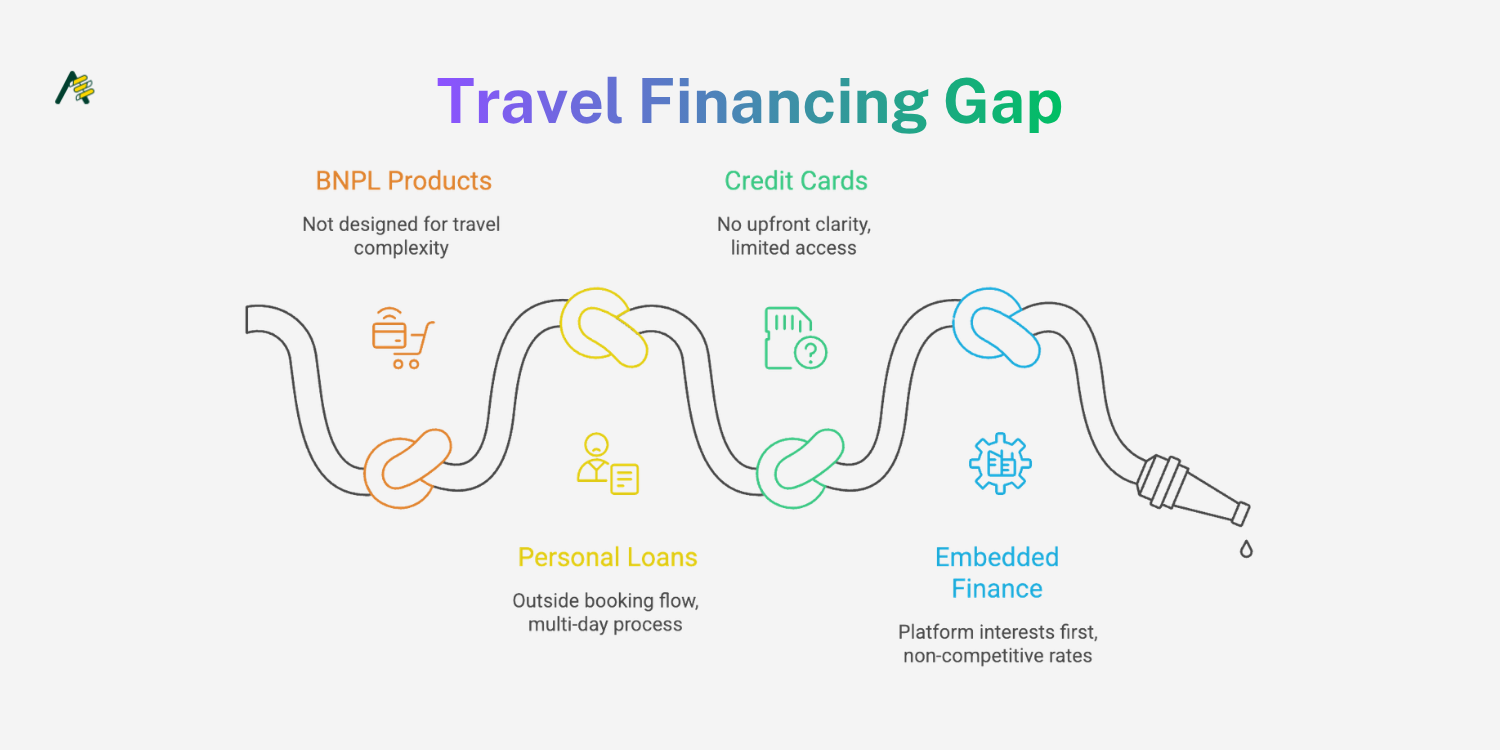

Why Existing Solutions Weren't Enough

The market wasn't short of options. It was short of options that worked for this specific context.

Buy-now-pay-later products, popular in retail, weren't designed for the complexity of travel bookings. They work well for a single SKU at a fixed price. A trip itinerary with flights, accommodation, and changing fares is a different problem entirely.

Personal loan products operated outside the booking flow. A user had to leave the travel platform, apply separately, wait for a decision, and return with funds - a multi-day process for a purchase that could take merely 20 minutes to decide.

Credit cards offered flexibility but no upfront clarity. A user didn't know what was available to them, or at what cost until they attempted to pay. And for users without high-limit cards, the experience ended at checkout.

Embedded finance tools from travel platforms existed, but served the platform's interests first. Rates were rarely competitive, the experience was transactional, and there was no reason for a user to prefer the platform's financing over their own bank.

None of these addressed the root issue: the gap between when someone decides they want to travel and when they know they can afford to. Paays needed to build something that closed that gap - not at checkout, but at the very beginning of the journey.

The Solution

PreQ was built on a single reordering of events: the loan comes before the destination, not after.

Instead of financing being the final hurdle in a booking flow, it became the starting point:

Users learnt their borrowing ceiling before they started browsing.

They shopped with a known budget.

The emotional and financial decision happenned together, not in sequence.

Alongside the loan, Paays layered in a deals ecosystem - exclusive pricing from partner vendors, available only to PreQ users. This changed the value proposition from "I need help paying for this trip" to "I get better prices because I use Paays." The financing enabled the trip, and the deals made it worth choosing Paays to book it.

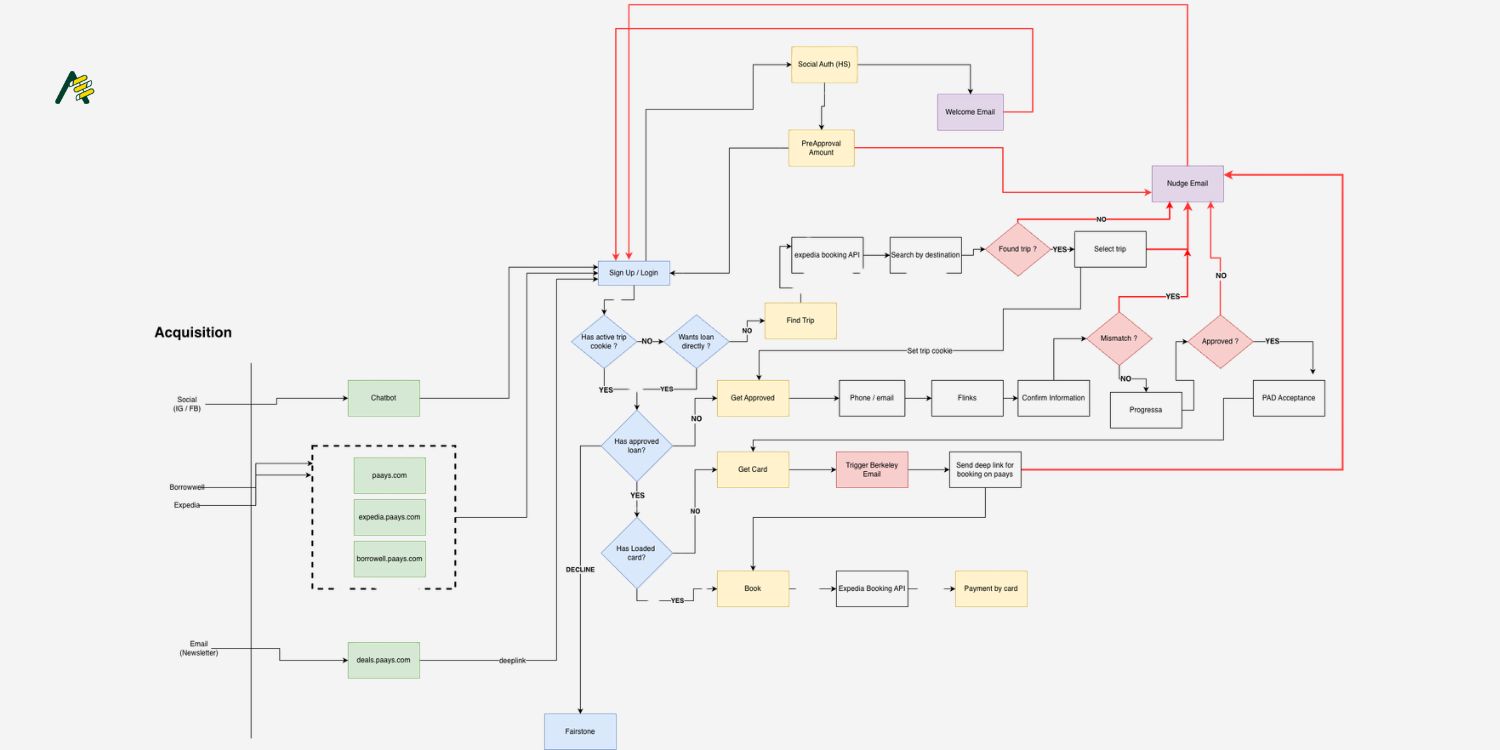

The platform served users across four acquisition channels - social media (Instagram and Facebook) via a chatbot qualification flow, co-branded partner micro-sites, direct referrals from Borrowwell and Expedia, and a deals-focused email newsletter. Each channel met users in a different state of intent, and the experience was calibrated accordingly.

Product Design

Onboarding and pre-approval

Users authenticated via Social Auth on entry, managed through HubSpot. Immediately on authentication, an open-banking connection was initiated through Flinks in the background - income and account analysis ran while the user moved through onboarding. By the time they reached the trip search, their pre-approval amount was ready and surfaced without any waiting state.

This sequencing was the product's most important UX decision. There was no holding screen, or "we'll be in touch." The number was simply present as a quiet ceiling that made browsing feel empowering. New users also received a welcome email on first authentication, establishing the Paays relationship before the first transaction.

Trip discovery

With a pre-approval amount in hand, users could search by destination through the Expedia Booking API, embedded natively within the Paays experience. No tab-switching, no session loss. When a trip was selected, a trip cookie was set, preserving the choice across sessions so a user who stepped away could return to exactly where they stopped.

If no trip is found, the system didn't stop in a dead-end. Instead, it triggered a nudge email that brings the user back when they're ready to look again.

The decision engine

After trip selection, PreQ ran three sequential checks to route the user to the right next step:

Has active trip cookie? Returning users resume immediately, with their trip pre-loaded and their pre-approval still valid.

Has approved loan? Existing loan holders skip the approval flow and proceed directly to card issuance. New applicants move through a lightweight verification sequence (phone, email, Flinks confirmation, information review) before going to Progressa for underwriting.

Has loaded card? Users with funded cards proceed to booking via the Expedia API and pay by card. Users with a card that hasn't been loaded receive a Berkeley trigger email with a precise deep link to the card-loading step.

Re-engagement

Every meaningful exit point in the flow routed to a tailored nudge email. The deep linking was specific: a user who dropped off at card loading landed on the card-loading screen, not the homepage, and thus their trip was saved. Their approval remained intact, and the only thing asked of them is to complete the one step they didn't finish.

This architecture treated abandonment as a pause rather than a failure. If someone started the process, they wanted to travel. The re-engagement system's job wasn't to sell them again - it was to remove whatever stopped them the first time.

Technology

PreQ ran on a small number of deep integrations, chosen because each one makes a specific step in the flow meaningfully better.

Partner Role:

Expedia Booking API: Live inventory, search, and booking

Flinks: Open banking - income and account verification

HubSpot: Social auth, CRM, email orchestration

Fairstone: Loan origination and servicing

Progressa: Underwriting and credit decisioning

Borrowwell: Audience referral and co-branded microsite

The most consequential integration was Flinks. Open banking was what makes real-time pre-approval without a hard credit pull possible - and that single technical decision was what enabled the entire "loan before destination" model. Without it, pre-approval would require a separate application session and introduce the delay that makes every competing product fall short.

HubSpot managed identity from the first touchpoint and orchestrates all email communication- welcome emails, nudge triggers, Berkeley Payment card-loading prompts - with sends tied to specific flow events rather than time-based drip sequences. That distinction mattered: emails arrived in context, when they were relevant, not on a schedule.

Progressa handled underwriting, with a mismatch-detection layer built in. When declared information didn't align with verified data, the system routed to a resolution loop rather than a rejection screen. Many mismatches were errors of input rather than indicators of risk, and treating them that way recovered approvals that would otherwise be lost.

Why This Approach Worked

Pre-approval reframes the shopping experience. Knowing your ceiling before you browse was a fundamentally different psychological state than discovering it at checkout. Users who shop within a known budget make faster decisions and abandon less frequently. The number isn't a limit - it's a permission.

Meeting users in the right channel with the right posture. A user arriving from Instagram is in discovery mode. A user arriving from Borrowwell is in financial evaluation mode. A user from the deals newsletter already has purchase intent. PreQ didn't funnel all of them through identical steps - it read the entry point and adjusted. That context-sensitivity was part of why conversion held up across very different acquisition sources.

The deals layer changes the category. An embedded loan product competes on rates. A platform that offers exclusive deals competes on value. By giving users a reason to come to Paays first - not just use it when they have to - the product created a pull rather than a push.

Re-engagement as infrastructure, not afterthought. Most products bolt on a re-engagement email sequence after the fact. PreQ built it in from the start, with precise deep links that restore session state. The result was a meaningful recovery of users who would otherwise have been written off as churned.

Key Lessons From This Project

The channel determines the mental model. Users arrive from different surfaces with different levels of intent and different expectations. Design that respects those differences converts better than design that collapses them into a single funnel. The entry point is a signal - use it.

Open banking is the unlock. The real-time, no-hard-pull pre-approval that makes PreQ feel magical is entirely dependent on the Flinks integration. In embedded finance products, the quality of the data connection determines the quality of the experience. This is the integration worth investing in.

Mismatch handling is a conversion lever. Information mismatches in underwriting are common and usually innocent. Building a resolution loop instead of a rejection screen recovered a meaningful share of approvals. The lesson generalises: whenever a flow has a binary pass/fail moment, ask whether the failure mode could be a recoverable state instead.

Deals aren't upsells - they're the headline. In user research, the partner deals were frequently cited as the primary reason someone chose Paays, with the loan as the enabler. When financing is positioned as unlocking better prices rather than enabling a purchase, the emotional framing of the product changes entirely. It stops feeling like debt and starts feeling like access.

Re-engagement is product design. Treating the nudge email system as a first-class product component - with event-based triggers, precise deep links, and session-persistent state - is what turns a drop-off into a recoverable moment. If it had been handled as a marketing email sequence, most of those users would have been lost.

Conclusion

The gap Paays set out to close - between the moment someone decides they want to travel and the moment they know they can afford to - was real, common, and consequential. It cost people trips they could have taken, and it cost the travel industry bookings that were already decided.

PreQ closed that gap by reordering the sequence: pre-approval first, destination second, booking third. By embedding that sequence into a multi-channel acquisition platform, layering in partner deals, and building a re-engagement architecture that treats drop-off as a pause rather than a loss, Paays created something that feels less like a financial product and more like a travel product that happens to include financing.

That distinction - felt by the user, deliberate in the design - was what makes PreQ worth building, and worth writing about.

PreQ launched to strong early traction before the COVID-19 pandemic brought the global travel industry to a halt. With borders closed and lockdowns in place, the product was shut down.

Adaptiv partners with ambitious product teams to design, build, and launch digital products. If you're working on something in fintech, travel, or embedded finance, we'd love to hear about it (hello@adaptiv.me).

Adaptiv Admin

@admin

Building the future of AI products at Adaptiv.Me.

More Articles

Case Study: How Magic Was Built to Make Paris Feel Smaller

Case Study: How Lama Was Built to Close the Gap Between Business Data and Business Decisions

Case Study: How Globist Is Building the AI Workspace To Kill the Marketing Tab Spiral

Case Study: How Ask Sétu Was Built to Guide Indian Students Through Every Stage of Life in France